Why Pay-per-Use Financing?

Recent years have shown market conditions to be increasingly volatile and less predictable. Add in supply chain issues and it becomes a real challenge for equipment operators to accurately forecast customer demand and plan production in the long run. Old and less efficient equipment worsens the problem with unexpected plant downtime and high energy use.

Effective balance sheet management is also impacted by the chosen financing solution. For example, under IFRS16, equipment and the corresponding liability must be booked on balance sheet when financing through traditional leasing. By contrast, Pay-per-Use financing generally qualifies as an operating expense, thereby supporting companies in having a leaner balance sheet.

Pay-per-Use financing increases financial resilience of businesses during production downtimes, low demand, or unexpected events and helps replace old equipment with new one whilst keeping CAPEX low. By assuming utilisation risk, Linxfour helps equipment operators focus on core competencies.

Frequently asked questions about financing solutions

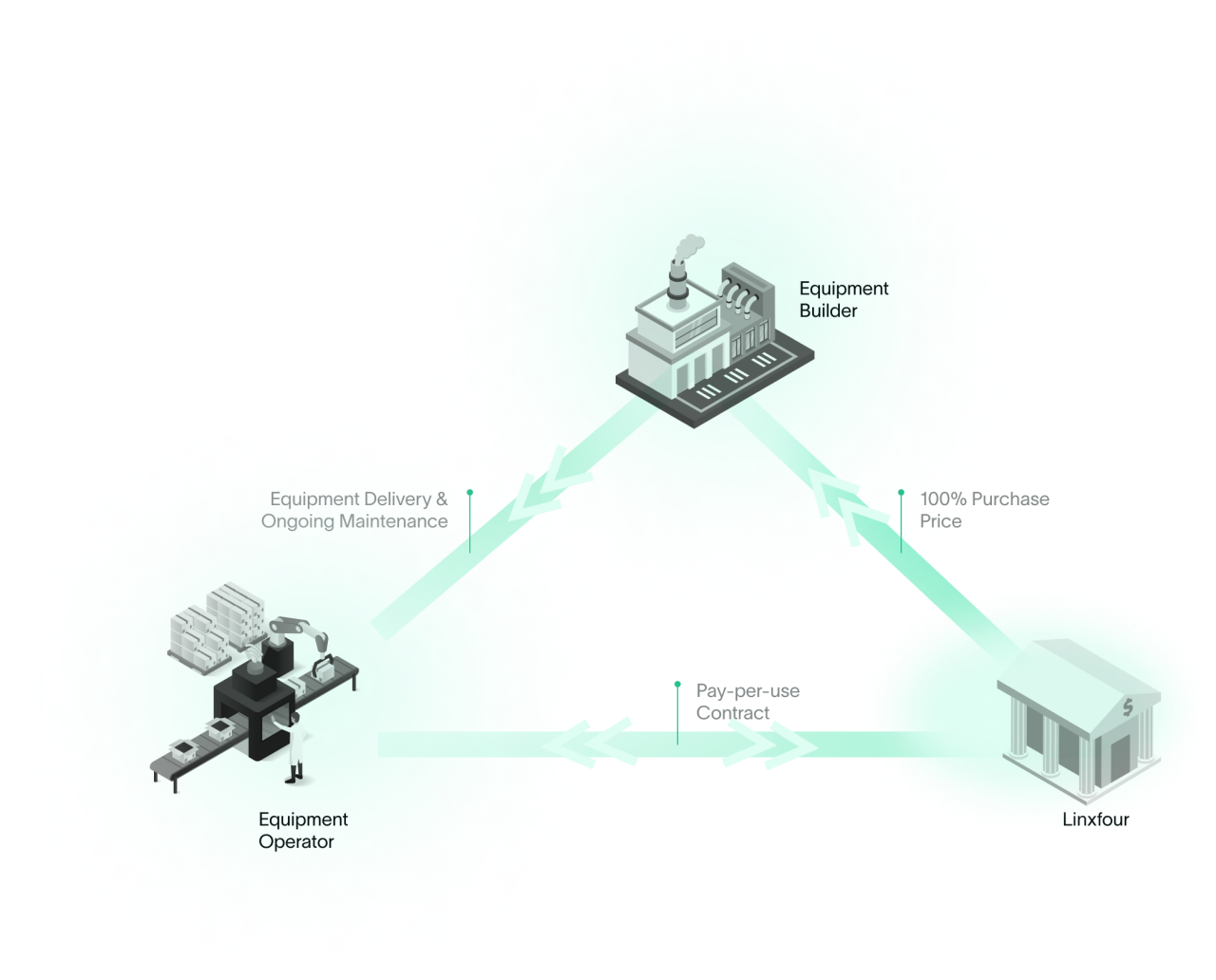

How does the Pay-per-Use process work?

After agreeing technical specifications and selling price, Linxfour sends an offer within 72 hours to the equipment operator. If the equipment operator agrees and passes credit checks, Linxfour and the equipment operator sign the Pay-per-Use contract. Linxfour invoices the equipment operator based on monthly usage, including all maintenance, insurance, and financing costs. At the end of the leasing contract, the operator can buy the equipment and become the legal owner.